Monthly Archives: February 2016

Week7_Susarla et al. (2010)_Aaron

Firms are increasingly relying on IT outsourcing to improve services quality and to lower in-house IT spending. However, practitioners and academics have seen high rates of failure in IT outsourcing due to holdup problems, which are represented as underinvestment and inefficient bargaining because of contract incompleteness. There is a tension on the understanding of holdup problems. One stream emphasizes the importance of clearly designed contract whereas the other believes that the nature of contract is incomplete.

Drawing on the argument from latter stream, Susarla et al.(2000) argue that contract extensiveness, defined as the extent to which firms and vendors can foresee contingencies when designing contracts for outsourced IT services, can alleviate holdup. Moreover, they argue while extensively detailed contracts are likely to include a greater breadth of activities outsourced to a vendor, task complexity makes it difficult to draft extensive contracts. Furthermore, extensive contracts may still be incomplete with respect to enforcement. They therefore examine the role of non-price contractual provisions, contract duration, and extendibility terms, which give firms an option to extend the contract to limit the likelihood of holdup. Using a unique data set over 100 IT outsourcing contracts, they test and support those arguments in their research model.

As to their contributions, first, they support the argument that contracts are fundamentally incomplete and suggest that non-price provisions play a strategic role in contracts design. Second, to extend the literature of contractual solutions to holdup problems, their findings suggest payoffs from repeated interactions between parties reduces the probability of inefficient bargaining. Last but not least, this study also complements prior analytical work by providing empirical evidence to understand how parties anticipate and design contingencies ex ante that are important to manage potential problems ex-post.

Gopal and Koka 2012_ Yiran

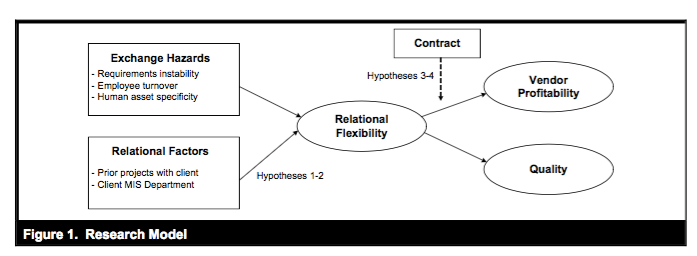

The authors examine the interacting effect of formal contracts and relational governance on vendor profitability and quality in the software outsourcing industry. They focus on the presence of relations flexibility in the exchange relationship, a critical manifestation of relational governance. They hypothesize that 1.relational flexibility provides greater benefits to an exchange partner that faces the greater proportion of risk in a project, induced through the contract; 2. The benefits manifest on the performance dimensions that are of importance to the risk-exposed partner.

The proposed the following model to test their hypothesis. They proposed two sub model: the relational flexibility model and the profitability and quality model. To operationalize the focal variable relational flexibility, they measure it as an observed outcome that represents ex post, extra-contractual aspect of the relationship. They identify five areas, namely payment procedures, warranty and liability conditions, installation and testing procedures, disputes resolution and project management. In terms of the dependent variables, the project profit was measured using the data collected from the company data base for each project. The service quality is measured by a five-item survey.

The author used muli-pronged analytic strategy to test the hypotheses. To solve the problem of the endogenous interacting variables, besides the OLS and 3SLS, they also use the Treatment effect model. All the hypotheses are supported, showing evidence for the argument that asymmetric benefits from relational flexibility to different contracting parties in an outsourcing relationship. The results also indicates that relational flexibility positively affects profitability in only fixed price contracts, where the vendor faces greater risk, while positively affecting quality only in time and materials contracts, where the client is at greater risk.

Week7_Susarla et al. (2010)_Ada

Key Concept:

Hold-up problem: In economics, the hold-up problem is central to the theory of incomplete contracts, and shows the difficulty in writing complete contracts. A hold-up problem arises when two factors are present:

- Parties to a future transaction must make non-contractible relationship-specific investments before the transaction takes place.

- The specific form of the optimal transaction (e.g. quality-level specifications, time of delivery, what quantity of units) cannot be determined with certainty beforehand.[1]

The hold-up problem is a situation where two parties may be able to work most efficiently by cooperating, but refrain from doing so due to concerns that they may give the other party increased bargaining power, and thereby reduce their own profits. The hold-up problem leads to severe economic cost and might also lead to underinvestment.

Motivation:

To improve service quality and to lower information technology cost, firms are fueled to increase their use of IT outsourcing. However, practitioners and academics realized that IT sourcing is fraught with difficulties and high rates of failure. One of the underlying risks comes from the hold-up problem. This paper uses a unique dataset to empirically examine this question.

Main findings:

- Task scope is positively and significantly associated with extensive contracts;

- Task complexity is negatively associated with contract extensive ness;

- Task complexity is negatively associated with long term contracts, which suggests that firms might be wary of the greater threat of inefficient bargaining posed by the vendor in a longer term contract;

- Task scope is positively associated with the presence of extendibility clauses;

- Task complexity is positively associated with extendibility terms in contracts;

- Contract extensiveness is positively associated with duration;

- Contract extensiveness is positively associated with extendibility.

Contributions:

This paper highlights that contracts are fundamentally incomplete and that nonprice provisions play a strategic role in contracts structuring. Drawing on literature that describes contractual solutions to the holdup problem, they argue that parties are motivated by payoffs from repeated interaction to undertake specific investment and to reduce the likelihood of inefficient bargaining.

Week 7_Langer et al. (2014)_Xinyu Li

In this paper, Practical Intelligence (PI), a concept from cognitive psychology as a supplement of academic intelligence, is proposed to be a critical factor for Project Managers (PM) to make their projects successful in software offshore outsourcing. Based on an information processing perspective, the paper posits that the PMs’ PI is positively related to project performance. Meanwhile, it also hypothesize that the PI-performance relationship is positively moderated by project characteristics categorized as project complexity (software size and schedule compression) and team complexity (team size and team dispersion), and negatively moderated by task familiarity (PM-task familiarity and team-task familiarity) and stakeholder familiarity (team member familiarity and PM-client familiarity).

This research adopts a mixed methodology to conduct empirical analyses. It obtains PI data of 209 PMs in a software service company through case studies, combined with dataset from the company’s archive data containing characteristics for each of the PMs and the projects they led. Proposed moderators are derived from the dataset using different analytic tools and models. The dependent variable project performance is measured separately by cost performance and client satisfaction.

The results from an OLS and SUR model verify the main effect of PI on project performance as well as most of the moderating effects. With certain limitation such as a progressive learning bias of PI, the paper contributes to related literature by 1) introducing and conceptualizing PI as an important capability for PMs, 2) identifying the characteristics of project context that moderate the PI effect on project performance, and 3) providing sufficient empirical evidence.

Week7_ Gopal (2012)_Yaeeun Kim

In the vendor-client relationship, how to govern the relation is important, however, the effect depends on the hazard. The study mentions two gaps. First gap is the moderating effect of risk exposure on the benefit of relational governance. According to the prior studies, in the presence of formal contracting, relational governance has a significant impact on the outcomes of economic activities. On the other hand, relational governance provides symmetric benefits to all parties. In a way of understanding the contradicting findings, this study focused on the positive effect of relation on mitigating risk. This suggests that the parties who take larger risks might be more beneficial as a result. Second, the effect of relational governance on enhancing values differed by the dimensions of outsourcing (e.g. quality and profitability). However, it is important to understand that when there is not equivalently expected hazard size, why would the other party would accept the relational governance if the party is not be a beneficent as the other party. Relational governance highlights flexibility in the environment of projects, resulting in more beneficial to immediate project rather than long-run project.

To test hypotheses, 105 projects was collected from a software service frim. The relational governance is inherently required for this area since software service firms outsource, and the relationship between the vendor and developer is important. From the findings, the study shows that relational flexibility positively affects profitability in only fixed price contracts, where the vendor faces greater risk, while positively affecting quality only in time and materials contracts, where the client is at greater risk. Service quality was measured by question items.

Overall, relational governance (relational flexibility) is beneficial for profitability depends on the type of contract. As expected, the effect of relational flexibility on profitability is moderated by FP contracts. However, the effect of T&M contracts was insignificant on the effect of relational flexibility on project profit.

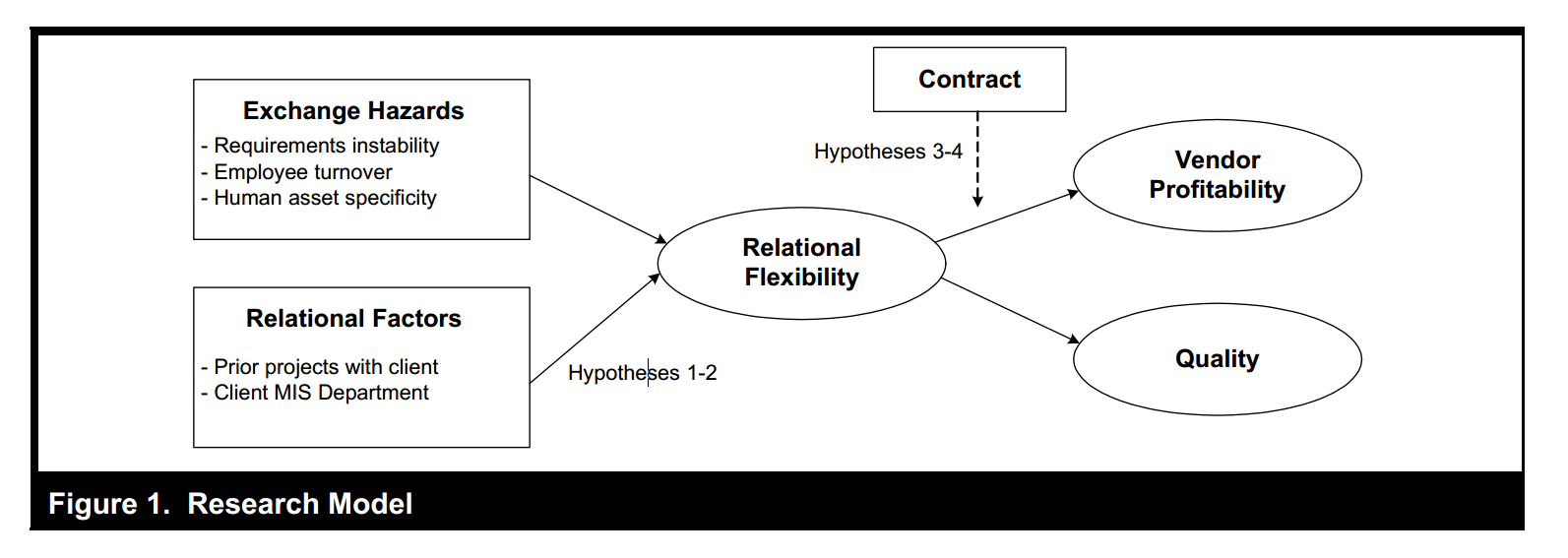

Week 7_Gopal and Koka (2012)_Vicky Xu

The Asymmetric Benefits of Relational Flexibility: Evidence from Software Development Outsourcing

Gopal and Koka (2012) examined how and when relational governance, operationalized as flexibility, provides benefits to exchange partners in the presence of formal contracts. They provided a more nuanced understanding of the relationship between formal and relational governance by contending. Gopal and Koka (2012) presented the conceptual model as the following (Figure 1, p. 559):

Gopal and Koka (2012) tested the hypotheses on a dataset of 105 software development outsourcing projects completed by an Indian software vendor. And they used a multi-pronged analytic strategy to test the hypotheses. The relational flexibility model included OLS, nonlinear 3SLS, and treatment effects. The Profitability and quality models include the interaction model, 3SLS, 2SLS, the non-interacted 2SLS, and the treatment effects.

Gopal and Koka (2012) found strong support for the hypotheses of asymmetric benefits from relational flexibility to different contracting parties in an outsourcing relationship. The findings in this paper highlight the need to establish risk exposure first, and then examine the effects of flexibility on performance contingent on risk exposure. And the findings also highlight the implications of relational governance for the performance dimensions of interest. The findings indicated that the need to incorporate a more nuanced, limited, and contingent view of relational governance and its benefits in extant theory, in contrast to the more expansive view of relational governance that predicts value for all partners to an exchange. What’s more, this paper also makes a methodological contribution.

However, this study has some limitations: (1). The data that from one vendor firm limits generalizability. (2). Dataset is small. (3). The measure of contract type is limited to the two extreme forms of contracts. (4). The measure of quality is perceptual and collected from the vendor. (5). The theoretical arguments used in this paper were based on the observed manifestation of relational governance in the specific exchange.

Week 7_Gopal et al.(2003)_Xue Guo

Contracts in Offshore Software Development: An Empirical Analysis

This paper is motivated by the tremendous growth of the offshore software development and the need to increase viability and profitability of vendor-client relationships. It empirically studies the determinants of contract choice in offshore software development projects and examines the factors that affect the project profits accruing to the software vendor.

The paper examines the adoption of the two prevalent forms of contracting in the software industry—fixed-price contract and time-and-materials contracts. The main risk will be borne by the vendor under a fixed-price contract, and the client under a time-and-material contract. Based on prior theories in contract, this paper presents four possible factors that may affect contract choice: software development risks, client knowledge set, bargaining power and market conditions. Empirically, most of the variables adopt measures from previous literature. In order to assess the reliability of the measurements, the paper uses multiple questionnaire items for one variable. The results show that project-related characteristics such as requirements uncertainty, project team size, and resources shortage significantly explain the contract choice in these cases.

Then the paper studies the efficiency of the contract by examining the effect of the information known during contracting on project profits and add three development factors to improve the fit of the regression analysis. The corresponding results show that vendor does make higher profits from time-and-materials contracts when control for other characteristics of the projects.

The contributions of the paper are that it empirically tests the determinants of contract choice in software industry and addresses the linkage between contract choice and project profits. However, the paper’s limitations are the restricted data set and measurement problem of some variable.

Week 7_Langer et al (2014)_Jung Kwan Kim

Langer, Slaughter, and Mukhopadhyay (2014) examine the impact of practical intelligence (PI) on project performance and the moderating effects of project complexity and familiarity. While the prior studies tend to specify formalized and widely-recognized management skills, knowledge, and experience of project managers, the authors bring up more subtle but dynamic capability, linking to the outcome of project.

Based on the in-depth data analysis on project progress and results in a leading software outsourcing vendor in India, the field study supports the following arguments:

- PM’s PI is positively associated with the increase in both cost performance and client satisfaction.

- The interaction of complexity with PI is significantly positive on the two types of project performance. In other words, when complexity of a project is higher, the impact of PI becomes stronger, leading to better performance.

- The interaction of familiarity with PI is significantly negative on the two types of project performance. That is, a project with low familiarity can harvest more benefits when a PM with high PI manage it.

Indeed, the supported arguments are intuitive and straightforward when we ponder upon the role of PI in a project management. The software outsourcing projects inevitably suffer from various factors that cause uncertainty and potential failure: requirement ambiguity, stakeholder conflicts, cultural misunderstanding, to name a few. PI basically helps a project manager resolve the critical, situational, and contextual problems, a capability that cannot be easily found or trained. A PM with high PI may be able to address the difficult problems, eventually bringing a higher chance of successful project results.

In conclusion, I think this study contributes much to the literature by finding the significant impact, the decent data source, and the parsimonious measure of PI.

Week 07 – Outsourcing – paper assignment

| Gopal et al. (2003) | Yea Eun |

| Gopal et al. (2003) | Xue |

| Susarla et al. (2010) | Aaron |

| Susarla et al. (2010) | Ada |

| Gopal and Koka (2012) | Vicky |

| Gopal and Koka (2012) | Yiran |

| Langer et al. (2014) | JK |

| Langer et al. (2014) | Xinyu |

Week 6_How to become a good teacher?

Discussion topic: How to become a good teacher?

Prof. Pang: I want to talk about teaching. I told you that teaching may not be as important as research in research schools, but it is still very important. I want you to think about your favorite teacher that you’ve met one by one and why that professor in your previous institution was a good teacher.

Student 1: One of my favorite teachers is from my master degree. He teaches data mining. He uses a lot of good examples to let us know how to use the different models; he also did surveys in our class.

Prof. Pang: So it’s like his class is more interactive. He lets you get involved in class.

Student 2: I want to share a story of one of my favorite teachers. He was also an advisor of mine. Beside he is knowledgeable, he is trustable, and he set a good example for us. He helped us solve problems not limited in academic but also in our life. We couldshare our study ideas and experience with him.

Prof. Pang: So he cares about students’ life and personal interests, beyond the classroom.

Student 3: My favorite teacher is from my undergraduate studies. He taught a supply chains analytic course. I think he is good in that he made many good examples to demonstrate some complex models. I took a very impressive course of his at the end of the semester. In that class, we did not have any real material. He told us why supply chain analytic is important pretty much like what you are doing in our seminar. I think at least that course did deeper teaching style than any other courses. Not only the class materials are important but also the philosophy of ideas is important.

Prof. Pang: He must have a very good ability to explain difficult stuff to students especially for undergraduates. That’s would be your job to explain technical or IT stuffs in the IS field to undergraduate students.

Student 4: I’d like to share my favorite teacher. He has a different background. I have some background with a history major during my undergraduate. I kind like the editor of the class. I remember a course named invisible city. He was facing a group of undergraduate. But he never stopped with half of class a break. He used one slice by another; it seems like the knowledge inserted into your body. This motivates me to be a professor. I want to be a professor that is knowledgeable like him.

Prof. Pang: So, I hope that you are going to become professors/teachers like them. Teaching is important. You won’t get tenured for becoming a super fantastic teacher. However, you still have to be a good teacher to survive.

Here is a kind of the criteria in most of the business schools. You have to get at least 4.0 out of 5.0 in your teaching evaluation. 4.2 to 4.3 out of 5.0 is good enough for tenure and a job market.

We are multi-taskers. We have to do many different works such as research, teaching, etc., and as our Dean says, we have to solve optimization problems every day. Here is an optimization problem(just consider research and teaching) to evaluate your value to get a job (or tenure):

Max V(R, T), R+T ≤ 24.

This illustrates that your value (in a job market or tenure) V depends on your Research and Teaching, but you don’t have unlimited time to spend in both. So you have to split your limited time between two. How you do it? It depends on the marginal returns from R and T, which is that the marginal return from R is much higher than from T. Therefore, we have to spend much more time on research to get more publish while spending not too much time on teaching, enough to get 4.2 out of 5.0 (at least 4.0 out of 5.0) in teaching evaluation.

The problem is however, that it is NOT easy to get 4.0! Let us think about an example where 10 students give you 4, 7 students give you 3, and 3 students give you 5. Then, your evaluation is 3.8. It looks like a good evolution but actually is not. You need to have more students who give you 5 than 3. We all know that we don’t go extreme (1 or 5) in filling out surveys. This is why it is not easy to get a good point like 4.0. And it is even more challenging for us, because we are not native speakers. You students won’t like your accent.

The bottom line is it is not easy to become a good teacher. Thus, it is very important to have teaching experience during your doctoral studies and to make efforts to become a good teacher.

There are several useful resources:

http://tlc.temple.edu Teaching and learning center

http://www.fox.temple.edu/cms_research/institutes-and-centers/center-for-innovation-in-teaching-and-learning/ Center for innovation in teaching and learning

http://tlc.temple.edu/teaching-certificates/teaching-higher-education-certificate-teachers-and-professionals Teaching higher education certificate teachers and professionals

Think about how to be a good teacher from now. I think it is a good idea to teach one course in your 3rd year after passing a comprehensive exam and becoming a candidate. I don’t think it is a good idea to teach in the 4th or 5th year, because you have to prepare your job market and dissertation. So the 3rd year is the best time to teach, and you have to prepare for that from now. You can sit in your professors’ class to take some of skills about how to teach, how to manage a class, how to interact with students, etc. Any question about teaching?

A few practical advices. We cannot get 4.0 when we just deliver lectures. My advisor said: “the more you talk in your classroom, the less evaluation you get”. So good teachers make students get involved. In my classroom, I ask a lot of questions. I want my students to talk more. It is more fun for them than to just listen what a teacher talks for the whole one hour or two. Good teachers care about students’ life, career, and interests beyond the classrooms. Good teachers have to have an ability to explain difficult stuffs to students. You have to get such a skill. That’s why I want you to share your favorite teachers because you have to become like them.

Also, there is a misconception that teaching and research are two separate things. I don’t agree with this. So my teaching approach is to use my research in my classroom and to deliver some theoretical perspectives/foundations to students. I think that’s our job as an academically qualified teacher.

Student 3: So if research can benefit our teaching, in what case can teaching benefit our research?

Prof. Pang: I got one of my research ideas from my class, which was about how to make balance between new IT development and IT maintenance. You can get research ideas from teaching. Teaching helps you keep the idea fresh.

Next week’s class – Thursday, Feb 25 at 9:30am

Next week, we will meet on Thursday, Feb 25 at 9:30am – noon at Speakman Hall 200.

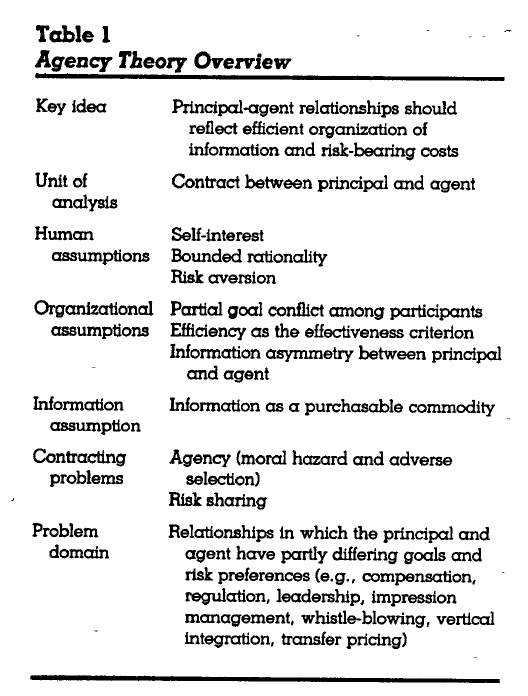

Agent Theory_Yiran

‘Agency Theory’

A supposition that explains the relationship between principals and agents in business. Agency theory is concerned with resolving problems that can exist in agency relationships; that is, between principals (such as shareholders) and agents of the principals (for example, company executives).

Week6_Xue et al (2010)_Xinyu

Driven by the contradictory empirical findings from extant literature, Xue et al. (2010) seeks to answer the question about the relationship between environmental uncertainty and centralization/ decentralization of IT governance. Because IT governance can be multidimensional constructs, to gain a better understanding of the relationship, this paper only focus on IT infrastructure governance.

Most of the prior research suggests environmental uncertainty will increase the decentralization of IT infrastructure governance because decentralization improves flexibility and responsiveness of business units which are crucial in uncertain environments. However, other theories such as agency theory suggests that decentralization in highly uncertain environments increases headquarters’ monitoring and evaluation costs, and also prevents efficient coordination and resource sharing among different business units. Therefore, this paper proposes a curvilinear relationship between environmental uncertainty and IT infrastructure governance, in which decentralization will increase as uncertainty moves from low to intermediate but will decrease as uncertainty moves from intermediate to high. In addition, the paper also proposes that the curvilinear relationship will be strengthened when business units and their headquarters are in unrelated business.

The unit of analysis in this study is business unit. There are three main constructs. The IT infrastructure governance is measured by a binary variable indicating whether the majority of IT infrastructure decisions are made by business unit managers. Environmental uncertainty is conceptualized by three dimensions—dynamism, munificence and complexity. Business unrelatedness is measured as the difference between a business unit and its headquarters’ NAICS industry codes. The model is constructed using a logistic regression. Both the curvilinear relationship between environmental uncertainty and IT infrastructure governance and the moderating effect of business unrelatedness are empirically confirmed.

Week6_Li et al (2012)_Xue Guo

The consequences of information technology control weaknesses on management information systems: the case of Sarbanes-Oxley internal control reports

This paper investigated the association between the strength of IT control over management information systems and the subsequent forecasting ability of the information produced by those systems. Sarbanes-Oxley (SOX) Act of 2002 highlights the importance of information system control related to the financial reporting systems. It hypothesizes and tests that management forecasts are less accurate for firms with IT material weaknesses in their financial reporting system (FRS) than the forecast for firms that do not have IT material weaknesses.

At first, the paper compared the management forecast accuracy for firms having IT material weaknesses with firms having either effective internal control or non-IT material weaknesses. Then the paper investigated whether certain categories of IT material weaknesses have a greater impact on the informational quality of the FRS than others.

The paper acquired the data from SOX 404 reports that available on Audit analytics from 2004 to 2008. The model uses management forecast error as the proxy for decision outcomes resulting from the quality of information produced by the FRS. The results show that firms with IT-related internal control material weaknesses have lower management accuracy than the firms have efficient internal control and have non-IT material weaknesses. And, when categorizes IT control quality into three dimensions: data processing integrity, system access and security, and system structure and usage, the paper found that data processing integrity has a greater impact on information quality than others.

One contribution of this paper is to highlight the implications of IT control on information quality issues for system users and decision makers. Also, the paper provides evidence that internal control reports, mandated by SOX, can provide information to system users about the underlying system and data quality.

Week6_Banker et al. (2011)_Vicky Xu

CIO Reporting Structure, Strategic Positioning, and Firm Performance

Since the previous studies on the CIO reporting structure is still unclear, and the pursuit of the ideal CIO reporting structure remains an unresolved issue both in the academic and also the practitioner IS literature, Banker et al. (2011) investigate the alignment or “fit” between the CIO (a.k.a. CTO) reporting structure and a firm’s strategic positioning, using business performance as the outcome of such alignment. The CIO manages IT within a firm, the responsibilities of CIO includes but not limited to managing IT resources, overseeing IT operation, involving firm strategy making, and improving firm performance.

Banker et al. (2011) address two research questions:

- How does a firm’s strategic positioning (differentiation or cost leadership) influence its CIO reporting structure (CIO reporting to the CEO versus to the CFO)?

- Is there an alignment or “fit” between the CIO reporting structure and the firm’s strategic positioning that is associated with higher firm performance?

Depending on the reporting structure, a CIO can either report to a CFO or a CEO within a firm. Depending on the business positioning strategy, a firm can be a product differentiator or cost leader. The authors consider two CIO reporting relationships that correspond to a firm’s strategy: (1) direct reporting to the CEO, enabling the CIO to use IT to support a differentiating strategy, or (2) direct reporting to the CFO, enabling the CIO to use IT to support a cost leadership strategy. The following table (Table 1, p492) shows the reporting structure and strategic positioning arrangement:

By analyzing the data set that collected by integrating data from two surveys, Banker et al. (2011) find out that the CIO-CEO reporting structure is more suitable for firms using the position strategy of differentiation; while the CIO-CFO reporting structure is more fitting for firms using the position strategy of cost leadership.

Week 6_Chatterjee and Ravichandran (2011)_Aaron

Decisions regarding inter-organizational information systems (IOS) ownership and control have been crucial for viability of these systems. Nonparticipation in IOS and IOS failure cause major concerns for practitioners but remain little understood academically.

Chatterjee and Ravichandran (2013) therefore investigate why and how firms seek ownership and control of IOS. They propose two distinct facets of IOS governance, transactional and financial governance, which represent firms’ financially responsibility for IOS and controls on transactions within IOS respectively. Drawing on resource dependence theory, they model the key motivators of IOS governance as resource criticality and replaceability, which affect IOS governance through their influences on operational integration existing between partners. Furthermore, they argue technological uncertainty moderates such influences.

Their model was empirically tested using data gathered from a survey of 159 US manufacturing firms. Through mediation analysis and mediated moderation test, they found that resource criticality positively affects the extent of financial and transactional IOS governance by increasing the needs for operational integration, whereas resource replaceability negatively affects them by reducing the need for operational integration. In addition, they also found technological uncertainty creates disincentives for IOS governance by weakening the positive influence of resource criticality on operational integration, but does not significantly affect the relationship between resource replaceability and operation integration.

Theoretically, this study contributes to understand the drivers of IOS governance choices made by firms, extends and complements the research stream on the role of IOS in fostering tighter buyer-supplier relationships. Practically, third party providers and technology vendors are suggested to create appropriate offerings by understanding the fit between firms’ IOS governance decisions and existing exchange arrangement. Moreover, firms seeking to leverage IOS for competitive benefits are encouraged to closely examine the contingencies that influence their supplier relationships before investing in these systems.

Week 6_Banker et al. (2011)_Jung Kwan Kim

Banker, Hu, Pavlou, and Luftman (2011) examine the CIO reporting structure and its impact on performance contingent on the alignment with strategic positioning. The prior studies in the information system literature have not identified the ideal CIO reporting structure. The authors argue that the ideal reporting structure should not be blindly established simply based on the strategic role of IT in a firm; the fit between a firm’s strategic positioning and its CIO reporting structure should be considered to secure higher performance, the authors contend.

To support the main argument, Banker, Hu, Pavlou, and Luftman (2011) posit the following hypotheses:

- H1: Differentiators are more likely to have their CIO report to the CEO.

- H2: Cost leaders are more likely to have their CIO report to the CFO.

Those hypotheses are theoretically and empirically well supported in that a direct access to a CEO may be helpful to convince the needs of risky IT initiatives to create differentiated customer value while a reporting to CFO may better promote the operational efficiency by lowering costs.

Now, the discussion of H1 and H2 naturally leads to the argument on the match between the strategic positioning and the reporting structure.

- H3: Alignment between strategic positioning (differentiation and cost leadership) and CIO reporting structure (CEO and CFO) is associated with a higher firm performance.

The long standing resource based view (RBV) buttresses the hypothesis in that complementary resources of a firm can be combined to produce higher performance.

In conclusion, the CIO reporting structure largely depends on the firm’s strategic positioning. Indeed, the reporting structure does influence significantly on the firm’s performance. However, the effect of the reporting structure can be materialized only conditional on the fit with the strategic positioning.

Week 6 Kirsch et al. (2002)_Yiran

Firms have begun to utilize a client liaison role as a means of fostering business unit ownership and leadership of IS projects, which exercise control of IS project leaders to ensure that IS projects make progress in conformance with the business value propositions and proposed schedules and budgets. This paper aims to examine the exercise of project control across the client-Is relationships that may take on a variety of forms (hierarchical and lateral settings). The author defined control as all attempts to motivate individuals to achieve desired objectives, and it can be exercised via formal and informal modes.

The research model suggests that the client liaison’s choice of control mode is dependent on behavior observability and outcome measurability. This relationship between antecedent conditions and control modes is moderated by the client liaison’s understanding of the information. Based this mode, four hypotheses are developed

HYPOTHESIS1. High levels of outcome measurability will be associated with the exercise of outcome control. (Supported)

HYPOTHESIS2. High levels of behavior observability and client’s understanding of the IS development process will be associated with the exercise of behavior control. (No interaction, but main effect)

HYPOTHESIS3. High levels of behavior observability and low levels of client understanding of the IS development process will be associated with the exercise of clan control. (Supported)

HYPOTHESIS 4A. Low levels of outcome measurability will be associated with the exercise of self-control. (Partial supported)

Data were gathered from a questionnaire survey of 69 pairs of clients and IS project leaders. Regression analysis was used for hypothesis testing. The results of this study provide support for most of the hypothesized antecedents of the exercise of control by client liaisons. The distinctive finding of this study is that high behavior observability is associated with the use of either behavior or clan control. However, the key limitation is the moderate sample size.

Week6_Chatterjee and Ravichanran (2013)_Ada

Governance of Inter-organizational Information Systems:

A Resource Dependence Perspective

Motivation:

Though IOS generated benefits have received much attention, less research has been directed toward understanding the reasons for the successes and failures of these systems. As decisions related to IOS ownership and control have always been crucial for the viability and survival of these systems, it is important to examine the factors that influence IOS ownership and control decisions.

Research Questions:

In this paper they investigated why and how firms seek ownership and control of IOS, which they labeled as IOS governance choices. Specifically, the research questions are:

- How do resource criticality and replaceability affect the financial and transactional IOS mediating by operational integration?

- How technological uncertainty moderate the impact of resource criticality and replaceability on the financial and transactional IOS?

Main Results:

- Resource criticality increased the need for IOS governance by positively affecting operational integration, while resource replaceability diminished the need for IOS governance by negatively impacting operational integration.

- Technological uncertainty negatively impacted the need for IOS governance by attenuating the positive effect of resource criticality on operational integration. However, results indicate that technological uncertainty failed to enhance the negative effect of resource replaceability on operational integration and hence failed to weaken the need for IOS governance as hypothesized.

Resource Dependence Theory:

Resource dependence theory (RDT) is the study of how the external resources of organizations affect the behavior of the organization. Resource dependence theory has implications regarding the optimal divisional structure of organizations, recruitment of board members and employees, production strategies, contract structure, external organizational links, and many other aspects of organizational strategy.

The basic argument of resource dependence theory can be summarized as follows:

- Organizations depend on resources.

- These resources ultimately originate from an organization’s environment.

- The environment, to a considerable extent, contains other organizations.

- The resources one organization needs are thus often in the hand of other organizations.

- Resources are a basis of power.

- Legally independent organizations can therefore depend on each other.

- Power and resource dependence are directly linked: Organization A’s power over organization B is equal to organization B’s dependence on organization A’s resources.

- Power is thus relational, situational and potentially mutual.

Week6_Li et al. (2012)_Yaeeun Kim

The greatest implication of this paper is oriented from testing the link between system quality and information quality, via actual decision making outcomes. They assess the forecast accuracy when IT material weaknesses are present. In short, firms with IT material weakness are associated with less accurate management forecasts. Improvements in IT control quality are associated with decrease in forecast error. Among the types of IT control problems, systems with IT control problems related to data processing issues are associated with low quality of decision outcome.

This empirical study, which used SOX 404 control reports, contributes to explaining the implications of IT controls on information quality issues for system users and decision makers. Just as manufacturing process focuses on managing the quality of input for enhancing the outcome, information systems focus on managing high quality of information for a better decision making.

The authors also examined the impact of the different dimensions of IT material weaknesses. From the findings, the authors showed that firms with IT material weakness have significantly larger management forecast errors, and the errors are larger than those of firms with non-IT material weaknesses, as problems in information systems could directly impact the FRS output data that management uses to form their forecasts.

Although IT controls are often correlated with the extent of overall control weakness, this study try to answer the remaining unclear points that which type of material weakness yields a greater impact on the quality of information produced by an information system. The control weakness is solely based on the firm’s SOX 404 reports. There are some limitations of this paper: Can the types of control weakness all be answered within this archival report? Also, it is hard to say that the severity of weakness is controlled across the firms.